Inflation at 0.5% – should we worry about deflation now?

Leave a commentJanuary 16, 2015 by Paul Goldsmith

So inflation has continued it’s fall to the point where deflation is a distinct possibility, with some economists saying it’s a probability. Yet nobody seems to be panicking? Should they be?

First of all, the facts. Inflation , as measured by the Consumer Prices Index, is now at 0.5%. This is the lowest it has been for 14 years. It should be a cause for celebration that we have inflation-less economic growth at the moment, as that should make the growth sustainable.

I wrote about the dangers of deflation not very long ago, and we do have to be careful not to be drawn into a deflationary spiral, in which people delay their purchases as they think prices are going to fall in the future, thus reducing demand, resulting in unemployment and more deflation.

That is unlikely to happen this time, because of the reasons for the current disinflation (inflation falling, remember, does not mean prices are falling, they are just growing slower).

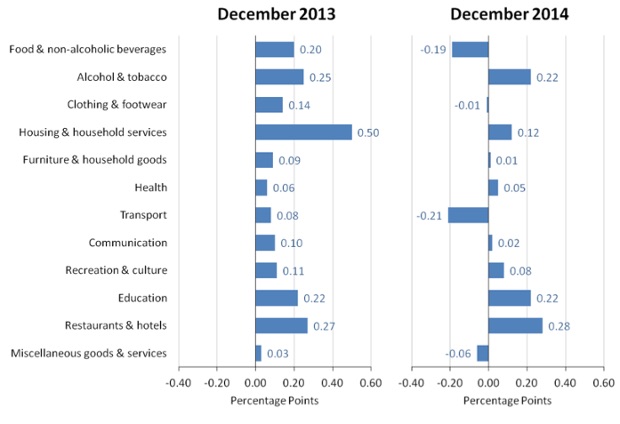

The fall in inflation is caused by a fall in oil prices, which means that the cost of transport has fallen, and by a fall in food prices, caused by the current supermarket price war.

The key to this is that inflation is falling because costs are falling, not because demand has fallen. Had it been the latter, then the Bank of England and the government would have been concerned. This is the situation the EU, where the ECB have even implemented negative interest rates in order to try and stimulate consumption.

Furthermore, the prices are falling for ‘necessities’ such as food and petrol, the purchase of which cannot really be delayed. Had they fallen for more ‘discretionary’ spending and that was getting delayed, such as on Televisions, then that may have been different. In fact, people may be MORE likely to buy televisions now as money is being freed up because people are having to spend less on necessities.

Some might argue in fact that Carney also believes, and this is important too, that any deflation would be temporary, not long-term, and that deflationary spirals occur when people think prices will fall for a long time.

There is one other question on this, and it is in the area of wages. Some have expressed concern that employers might use the smaller growth in the price level to justify a smaller growth in wages. That is certainly a possibility, but it is unlikely for two reasons: Firstly, we are in a period of economic growth, so employers are less likely to be looking to give overly parsimonious wage settlements. Secondly, unemployment is low, down to 6%, which means that employers are going to start to have to compete for employees, and offering low wages is unlikely.

Ultimately, the Bank of England didn’t rush into policy prescriptions when inflation was high, recognising that much of it was caused by costs rising rather than it being a demand problem, and it rightly felt that the inflation was short-term. So it is likely to see through this period of low inflation too.

Mark Carney still has to write his open letter of explanation to George Osborne explaining why the Bank of England’s inflation target (1% – 3%) has been missed. But I doubt he will be too apologetic, particularly as anything that makes the pound in the British public’s pocket go further around election time is something Osborne will encourage.